New Delhi: With the growing insistence to lower emission levels and enhance fuel efficiency in vehicles, besides reducing weight, theIndian tyre industryis embracing new trends in the manufacturing process to meet the changing market dynamics and cater to the latest demands of the OEMs (Original Equipment Manufacturers).

The heavy investment driven tyre industry contributes 3 per cent of the manufacturing GDP when the entire automotive sector accounts for 7.1 per cent of the GDP and almost 49 per cent to the nation’s manufacturing GDP (FY 2015-16).

The tyre makers in India are gearing up to intensify their role in the modernisation phase, largely driven by demand and supply conditions as also directly proportional to automobile sales to some extent.

The tyre makers in India is gearing up to intensify its role in the modernisation phase.

The tyre makers in India is gearing up to intensify its role in the modernisation phase.

Besides, with increasing focus on corporate average fuel efficiency (CAFE) norms to curb the alarming levels of pollution, companies have immense pressure to build products which have minimal friction and offers higher fuel efficiency.

In this direction, the tyre manufacturers have been grappling to alter manufacturing mechanisms to meet changing trends and demands.

Latest trends in the industry include finer tolerances in the manufacturing process, inclusion of more radials which consume less fuel, low rolling resistance and focus on better traction and on road performance which increases fuel efficiency.

A radial tyre allows the sidewall and the tread to function as two independent features of the tyre. A bias tyre consists of multiple rubber plies over lapping each other. The crown and sidewalls are interdependent.

The companies are stepping up the manufacturing facilities with technologies that improve heat development in tyres with effort towards less usage of carbon black, which in turn contributes in lowering emissions.

Other impactful trend in the manufacturing of tyres include usage of higher component of ‘silica’ which helps in the manufacturing process and in improving tyre performance by lowering the rolling resistance as well as improving cut and chip resistance.

“Tyre manufacturing and tyre performance are directly linked to the emission levels. In our tires we promote radials which consume an average 8-10 per cent lesser fuel while working and hence thereby lesser pollution,” said Vidit Jain, Chief – Technology and R&D, Alliance Tire Group (ATG).

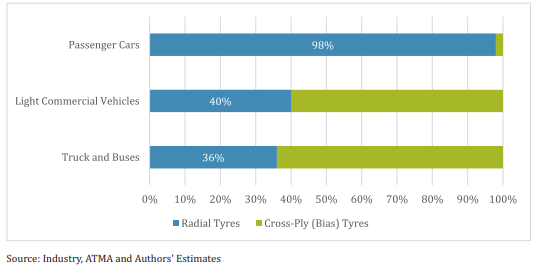

The passenger car tyre segment has radialisation of over 98 per cent, while its only 35 per cent in truck and bus segment and 40 per cent in light commercial vehicles tyres.

(Usage of Radials in various segment)

Latest trends in the tyre industry include inclusion of more radials which consume less fuel.

Latest trends in the tyre industry include inclusion of more radials which consume less fuel.

He further said the company is ensuring that its tyres provide the best traction and on road performance which in turn increases fuel efficiency and low rolling resistance in the tire and lightweight also ensures that lesser fuel is consumed by the vehicle.

ATG is a fully owned subsidiary of The Yokohama Rubber Company (YRC), Japan.

With regard to usage of silica, he said, “Silica helps in manufacturing processes as well as in improving tyre performance by lowering the rolling resistance as well as improving cut and chip resistance. We use many grades of Silica in most of our tires.”

Echoing similar sentiments, Pirelli Tyres Commercial Director Akash Singh Rathore said, the company is adopting the latest trend which calls for lower usage of carbon black and more silica content do increase the fuel efficiency and reduce pollution.

“Over the years, in our manufacturing plants, the usage of carbon black has significantly gone down in the tyres that are made for passenger vehicles,” he told ETAuto at the Tyre Expo here. “For commercial vehicles, we need the right amount of carbon black as those tyres need to manage the pressure of the heavily loaded vehicles,” he added.

Also Read: ‘Auto component industry to grow at 10-12% CAGR in long term’

Industry analyst are of the view that the tyres made for passenger vehicles, two and three-wheelers need not have too much of carbon black as they do not have the bear the load as much as a commercial vehicle needs to.

Since these segments form a majority of the automobile sales, higher usage of less harmful raw materials such as silica can tremendously help in lowering pollution levels.

Tyre dealers in the NCR said there has been a massive change in the design and weight of the tyres now made by the manufacturers as compared to five to seven years back.

“For a tyre made for and ideal sedan, the weight has gone down by about 2-3 kgs than those made during 2012-13 and similar is the case with two and three-wheelers,” said one of the dealers.

However, in the commercial vehicle space, particularly in the Medium & Heavy Commercial Vehicle (M&HCV) segment, the hasn’t been much change in the last few years.

Another dealer of commercial vehicle tyres said, “In this area, no major transformation can happen in terms of lightweighting as the requirements of those vehicles are such that the tyres have to be heavy to sustain on Indian roads and travel long distances”.

Market Dynamics:

Tyre demand originates from two end-user categories — OEMs and the replacement segment. Demand from the replacement segment dominates the Indian tyre market contributing about 56 per cent of the total volume, while the OEMs account for the rest 44 percent.

Consumption by OEMs is dependent on new automobile sales trend while the replacement segment is linked to usage patterns and replacement cycles.

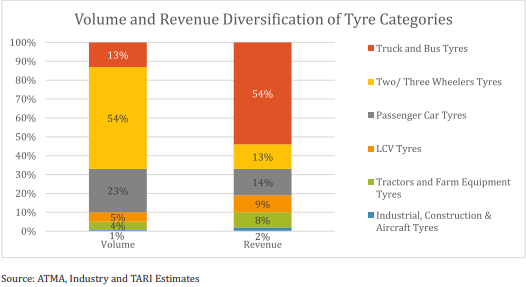

In the overall sales of tyres in unit terms, the commercial segment contributes about 21 per cent while the remaining comes from sales of personal vehicles which includes passenger vehicles, two and three wheelers.

Under personal segment, two and three wheelers constitute about 55 per cent sales while the passenger cars made up for the balance sales.

Tyre demand originates from two end-user categories — OEMs and the replacement segment.T&B (Trucks&Buses) dominates overall commercial usage segment with followed by LCV segment. Tractor front and rear tyre segment constitute the remaining

Tyre demand originates from two end-user categories — OEMs and the replacement segment.T&B (Trucks&Buses) dominates overall commercial usage segment with followed by LCV segment. Tractor front and rear tyre segment constitute the remaining

Top 10 companies account for about 80 per cent of the market share. Top three companies — MRF, Apollo Tyres and JK Tyres — have 55 per cent of the market share of the Indian tyre industry and figure among the top 25 global companies in terms of revenue.

Raw Material:

The tyre is an assembly of numerous components that are built up on a drum and then cured in a press under heat and pressure.

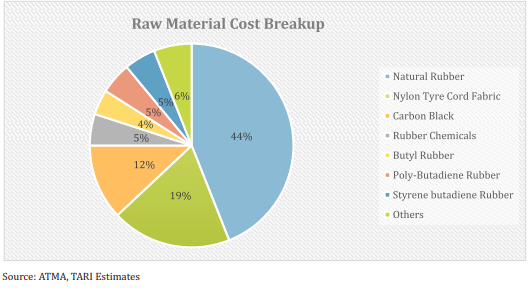

Raw material cost forms the largest cost head in the tyre industry accounting for about 65-70 per cent of the total. The main raw materials used to manufacture tyres are natural rubber, poly butadiene rubber (PBR), styrene butadiene rubber (SBR) and nylon tyre cord fabric.

Rubber is a major component in manufacturing of a tyre. There are three categories of rubber used in the manufacturing process viz natural rubber (NR), styrene butadiene rubber (SBR) and poly butadiene rubber (PBR).

Rubber including (natural and synthetic), nylon tyre cord fabric (NTC) and carbon black constitute a significant portion i.e. 60-65 per cent of the overall raw material cost of the industry, Care Ratings said, adding hence any change in the prices of these materials impact the overall industry’s profitability.

Rubber is a major component in manufacturing of a tyre.

Rubber is a major component in manufacturing of a tyre.

The price of rubber is prone to fluctuations and in the previous fiscal year, domestic and international rubber prices increased by about 28 per cent. It had declined by 24 per cent and 15 per cent y-o-y for previous two consecutive years.

The reason for high natural rubber price in the domestic market is due to the demand-supply gap in production and consumption of rubber in the country. Competitive prices in the international market also leads to high imports.

Exports:

Tyre exports are estimated to grow by 8-10 per cent over the next three years led by stable demand and increased acceptance of Indian tyres in overseas markets, both in terms of quality and pricing. It was around 9 per cent in FY 2018.

However, with rising penetration of low cost Chinese tyres in overseas markets, especially post the removal of anti-dumping duty (ADD) by the US on the Chinese tyres in February 2017, competition from China (both in terms of volumes and pricing) will remain a key challenge, as per and ICRA note.

For FY 2019, the unit and tonnage growth is pegged at 8-8.5 per cent and 6.5-7 per cent, respectively.

Currently, India’s contribution to the global tyre trade is USD 1.5 billion (1.72 per cent) out of the $80 billion market. ATMA expects export sahre to increase to about 5 per cent given that the industry is highly competitive and there is a headroom for tyre exports.

Top destinations for exports include US, Germany, France, UK, Italy, Spain, Turkey, Netherlands, UAE, Brazil and Australia.

The US and EU countries are the top potential markets for exports, and the driving factor would be the Government signing trade agreements with these countries which can provide concessional tariff for tyres.

Challenges:

A DIPP report highlights that rubber (tyres) is one manufacturing industry thathas been affected by large imports from China. Due to a slowdown in the Chinese economy, their tyre manufacturers often dump their products in the Indian market which affects the domestic industry.

Although the government has imposed anti-dumping duty, but that is based on loss of profit and is not a deterrent.

Besides, reports suggest that illegal or illicit imports are also a cause for concern.

The share of imports from China has gone up to over 50 per cent from just about 20 per cent in the last five years, as per the data available with Automotive Tyre Manufacturers Association (ATMA).

Due to rising imports, the domestic industry has been lingering with decline in production and the capacity utilisation of plants has remain subdued.

Other challenge in India is the inverted duty structure for the tyre industry which adds pressure to the players. Analyst said the duty structure needs to be corrected by increasing the customs duty on tyres to keep it at par with the duty attracted by natural rubber, which will help the domestic industry to be competitive.

Inverted duty structure is where the key raw material attracts higher customs duty than the finished product. In this case natural rubber attracts more customs duty than the completely built tyres.

Also, import of natural rubber needs a prior license and declaration, which increases holding costs making the tyre industry non-competitive.

Furthermore, trade agreements have affected the domestic industry as concessions are provided on customs duty on finished tyres from countries with which India has an FTA (Free Trade Agreement) but not on natural rubber. Natural rubber falls under the negative list and therefore it increase the cost of tyres made in the domestic market.

Besides, the corporate income tax in India is higher than many other countries, which reduces competitiveness in the Indian tyre industry.

In terms of raw material, both natural rubber and crude are controlled by the external environment and little can be done to control the raw material price movement.

Company Financials:

Even after the challenges mentioned above, the tyre companies have managed to remain profitable in the Indian market. However, the potential of growth is almost two times than what it is now if the hurdles are taken care off.

1> Top in the chart is MRF Ltd. The company’s total income (net of excise duty) was Rs 15,104.40 crores for the year ended 31st March 2018, an increase of 11.22 per cent as compared to Rs 13,580.83 crore in the previous year. The Profit before tax stood at Rs 1,601.91 crore for the year ended 31st March 2018, as against Rs 2,066.37 crore for the previous financial year.

After making provision for income-tax, the net profit for the year ended 31st March 2018 was Rs 1,092.28 crore as against Rs 1,451.08 crore for the previous financial year.

The company’s export for the year ended 31st March 2018, was Rs 1,353 crore as against Rs 1,316 crore for the previous year ended 31st March 2017.

2> Apollo Tyres Ltd — The company’s net sales for the full year witnessed a growth of 12 per cent, as compared to the last fiscal, to close at Rs 14,674 crore. Net profit reported for the full year of FY 2018 was Rs 724 crore.

Both, Indian and European Operations, continued with their growth momentum and registered a revenue growth led by a strong performance in the commercial vehicle segment, especially truck radials, in India, and passenger vehicle category in Europe. Apollo Tyres Ltd operating profit for the financial year 2017-18 stood at Rs 1,768 crore.

3> JK Tyre & Industries Ltd — The company’s net revenue for the year at Rs 8,272 crore, an increase of 8 per cent. Operating Profit for the year was Rs 883 crore and Profit Before Tax (PBT) for the year was Rs 107 crore on consolidated basis.

In the year 2017-18, the sales volumes at JK Tyre grew by 11 per cent. On standalone basis, the total income during the previous financial year stood at Rs 6,510.95 crore. Truck/Bus radialisation which JK Tyre had pioneered, further accelerated to 47 per cent during the year.

JK Tyre has global presence in 100 countries across six continents, backed by production support from 12 plants – 9 in lndia and 3 in Mexico.

4> CEAT Ltd: The company’s consolidated profit during the 2017-18 financial year stood at Rs 233.29 crore. Total income during the last financial year was Rs 6,429.14 crore.

Profit Before Tax (PBT) was reported at Rs 367.32 crore in the fiscal 2017-18. The company has total assets worth Rs 5,160.99 crore as on March 31, 2018.

Outlook:

As per reports, Tyre OEM segment is expected to witness higher growth in the next two fiscals fuelled by robust automobile sales.

The fuel prices were on the rise for quite sometime now but have been on a decline for the past two weeks. Therefore, with expectations that the price will go down besides lower cost of ownership of vehicles, push on manufacturing and higher infrastructure spend is expected to result in further growth of the automobile sector.

With stable automobile sales, the tyre industry is set to gain in the OEM space.

A Care Ratings report said tyre manufacturers supplying to Commercial Vehicle, Passenger Vehicle, and Tractors segment are expected to benefit the most in the near term as the outlook for these auto segment in the Indian Market is relatively more positive.

With stable automobile sales, the tyre industry is set to gain in the OEM space.

With stable automobile sales, the tyre industry is set to gain in the OEM space.

On the other hand, the report suggested by FY 2019, about Rs 70 billion worth projects are to be completed adding another 12 million unit capacity to the industry. Going forward, significant capex will put pressure on the utilisation levels and hamper the operational margins of the players.

Analyst said sales are expected to grow about 10 per annum and domestic and export demand for tyres is expected to remain robust during this period on the back of strong growth prospects for Auto OEMs as well as the stable replacement market.

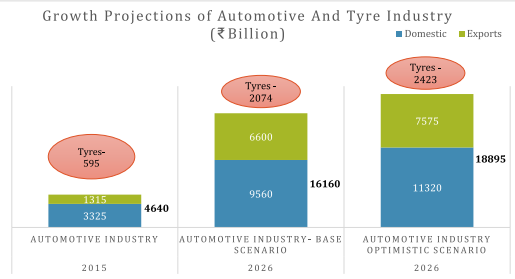

ATMA said the tyre industry being an integral part of the automotive industry is likely to reach levels of Rs 2,074-2,423 billion by 2026.

The Government of India and Indian Automotive Industry has developed a collective vision plan referred to as ‘Automotive Mission Plan 2016-26–AMP 2026’.

The AMP 2026 aims to propel the Indian Automotive Industry to be the ‘Engine of the Make in India Programme’.

The objective of AMP 2026 is “where the vehicles, auto components and tractor industry should reach over next ten years in terms of size, contribution to India’s

development, global foot print, technological maturity, competitiveness and institutional structure and capabilities”.

Employment:

The Annual Survey of Industry (ASI), MOSPI data reveals that the tyre industry provides direct employment to more than 0.15 million people, which is about 0.12 million in the organised sector. It also provides livelihood to over 1 million people such as retreaders, dealers and repairers directly and indirectly associated with the industry.

Further, employment generated by the industry in services such as tyre repairing, air filling, etc is also very significant.

(Source: Care Ratings, ATMA)